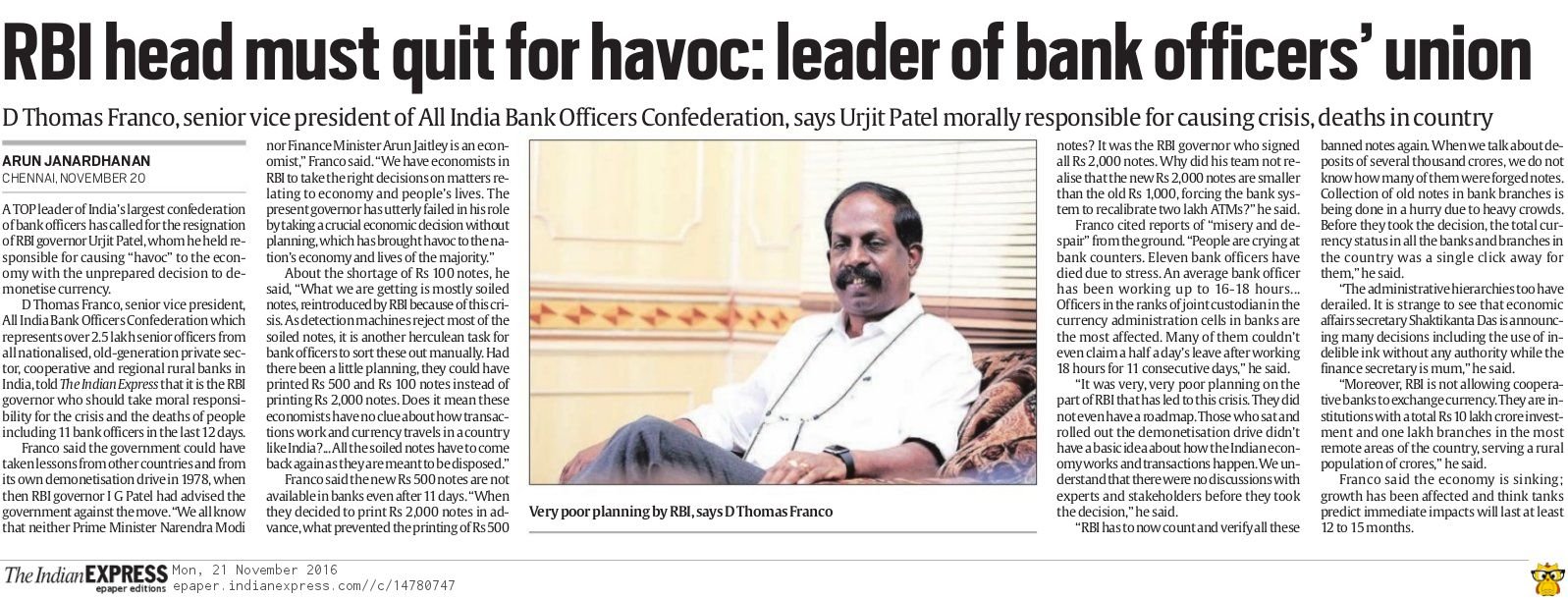

he implementation of the demonetisation exercise is unsatisfactory and the Centre is framing rules as it goes along

SOMETIMES A SHOCK TO THE SYSTEM EFFECTS BEHAVIOUR CHANGE FAR BETTER THAN ANY OTHER MEANS. THIS MAY NOT WORK EVERY TIME AND NOT EVERYONE CAN PULL IT OFF

On November 8, Prime Minister Narendra Modi made an unscheduled televised address to the nation at 8 pm. No one had any idea what he was going to talk about. Sure, there had been rumours of a new ₹2,000 denomination banknote in the works — many of the rumours gave this new currency note near mythical properties — but no one expected Modi to speak about that.

RAVI CHOUDHARY/HTThere has been inadequate supply of cash at banks, not enough of the new notes are being printed, there’s some amount of panic, and agricultural markets and packaged goods distribution chains have been hit

As it turned out, the ₹2,000 denomination note did feature in the prime minister’s speech during which he announced what was effectively a demonetisation exercise by rendering existing ₹500 and ₹1,000 denomination notes invalid.

It has for long (and frequently) been argued that scrapping high-value notes will hamper, if not altogether stop (even if only temporarily), transactions in the parallel economy.

“The $100 bill accounts for almost 80% of the US’ stunning $4,200 per capita cash supply. The ¥10,000 note (about $100) accounts for roughly 90% of Japan’s per capita cash holdings at almost $7,000. And, as I have been arguing for two decades, all this cash is facilitating growth mainly in the underground economy,” Kenneth Rogoff, professor of economics and public policy at Harvard, wrote in September.

In India, high-value currency (₹500 and ₹1,000 notes) accounted for 86% of cash supply.

“Higher denomination notes are particularly useful to criminals and tax evaders. What if we demonetised the high value notes?,” economist Ajit Ranade asked in a March column in Mint.

The man widely credited as having influenced Modi to do this, social activist Anil Bokil of Arthakranti (it means economic revolution, which should leave no one in any doubt about his motives), has for long campaigned for such demonetisation.

Enough has been written about the fallout of Modi’s announcement. There has been inadequate supply of cash at banks, not enough of the new notes are being printed, there’s some amount of panic, and agricultural markets and packaged goods distribution chains have been hit.

It is clear that the implementation of the demonetisation exercise has left a lot to be desired. The government seems to be framing rules as it goes along and that is never a good thing. A government official told me that the announcement had been rushed because buzz about a new currency was gaining momentum, especially in social media, and the government was worried that news of the demonetisation would soon be out. Indeed, some conspiracy theories allege that several people knew about the demonetisation and benefited from this knowledge.

There has also been analysis of how the exercise could result in windfall gains for the government (not true, as Ranade wrote in Mint recently), a contraction in the economy (too early to say), or lower interest rates (perhaps; banks are now flush with funds and may well be able to better transmit the central bank’s interest rate cuts). It is also, despite arguments to the contrary, what analysts would call a “net negative” for anyone with unaccounted-for cash.

To me, it is clear that Modi has banked on his personal equity to effect a behaviour change. Indians, even those with credit cards and payment apps, use a lot of cash. Demonetisation has forced them to resort to plastic and apps. It is likely that at least some of them will continue to do so even after the current cash crisis ends. It is also clear that the demonetisation exercise will increase usage of formal banking channels by many people who currently do not have bank accounts or do not use the ones they have.

Sometimes a shock to the system effects behaviour change far better than any other means. Sure, this may not work every time and not everyone may be able to pull it off but Modi is evidently gambling that he can. What now? The government will have to follow up and put in place measures to curb the creation of black money. Solving the election-funding puzzle is part of that and Modi did air his thoughts on the State funding of elections last week.

There have also been rumours about a possible rationalisation of income tax rates and a banking transaction tax to replace income tax.

The first is a good idea. The second, again suggested by Bokil, is not such a good one as Mint pointed out in an editorial in early 2014 when the idea seemed to be gaining support in BJP and RSS circles.

Still, with Modi in charge, anything is possible.

‘Note ban will lead to six months of chaos’

Former RBI deputy governor KC Chakraborty has come down heavily on the demonetisation exercise, adding it will lead to chaos in the next six months unless there is efficient replacement of currency notes. The outspoken former banker recently spoke to HT on the issue. Excerpts.

Can demonetisation curb black money?

Currency to the tune of ₹17 lakh crore is not black. If it goes into the hands of people who don’t pay taxes, it becomes black. If a taxpayer gets the money, it turns white. What we are killing is the note. We are not catching people who have not paid taxes. For that you have the I-T department, but they are not doing their duty. The poor hoard cash. The rich, who don’t pay taxes, don’t keep the black money under their pillows.

How much black money do you think is in cash?

Suppose there is 20% black money in the economy and of the total money supply, currency is only 10%, this means that 10% is black money. I feel that the rich move black money very fast as there are leakages. By banning notes, you are only increasing costs and taking away the right of the common man.

How can this be managed?

If your enforcement department, I-T , is weak, it cannot be managed. It is an administrative issue. You think income tax officials don’t know who hold black money? Next six months will be chaotic. It depends on how efficiently you bring back currency. If there is enough cash, why the restriction on withdrawals?

The UPA also planned to demonetise currency notes, but the RBI rejected the proposal. Why?

Yes. We thought it should not be done. That’s it.

How much black money is there in real estate?

People say that 20% of the economy is black money. In that case, black money constitutes 20% of all sectors. Its share is even higher in gold (40%) and real estate. But even the poor purchase gold.

What can be the negative impact?

The economy will suffer because liquidity has been sucked out. You have stopped market transactions for 70% of the economy. Even black money holders will not spend. The poor will suffer more. Already we can see farmers and small businesses are hit.

But banks are now flush with cash …

That (₹500 and ₹1,000 notes) is ultimately scrap paper now. The RBI will take six months to replace these and banks will have to pay 4% interest on those deposits. Only some time later, banks will be able to lend. There is no credit demand from the rich.

What about NPAs?

The NPA situation is very bad. All efforts should be made to identify the NPAs. If a person is sick, the person is not the problem. The problem with the NPA is the equity. Here no industrialist is doing business with his own money. It requires a surgical operation and we are administering small doses of tonic.

Will S4A (Scheme for Sustainable Structuring of

Stressed Assets) help?

It is bogus. The medicine is being given so that the person is not declared sick. The fellow who is sick needs more medicines. I (as a bank) am constantly trying to avoid the classification of NPAs. There is nothing sustainable and unsustainable. A person cannot be half sick. This is manipulation.

All NPAs should be identified. They are still hiding it. The RBI has said restructured debt will be NPA. When unsustainable debt gets converted into equity, it is the restructuring of an asset, which means it’s an NPA. If a bank thinks it can recover the money, why write it off. These write-offs are the biggest scandal of the century (and) must be stopped immediately.

But banks say entire provisions have been made and loans are being removed for accounting

You are an NPA, you are not ashamed of that, but showing it to other people is bad? If the economy improves, we will be better off, but banks need to perform.